The Psychology of Money Chapter 1: No One’s Crazy

- Kevin Giammalva

- Jul 15, 2025

- 2 min read

Updated: May 7

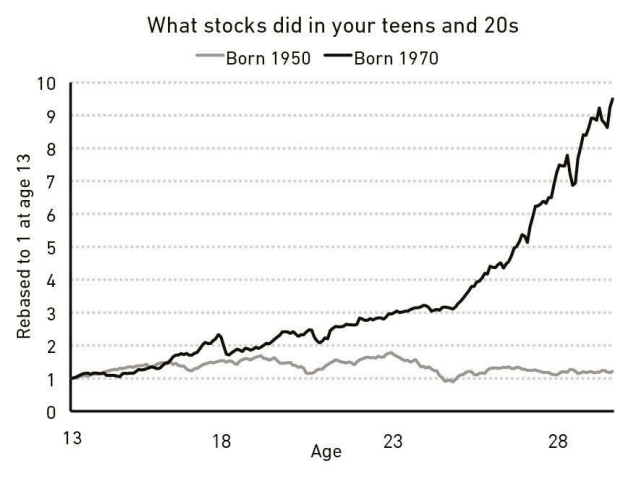

What do you remember about the U.S. economy during your teens and twenties? It’s not likely that you started tracking DJIA at this age, but maybe you remember headlines during these years related to inflation, economic turmoil, or unprecedented growth.

Would you be surprised that, on average, how we think and feel about our own finances is largely influenced by what the economy was doing during those formative years? See two charts below from The Psychology of Money.

If you were born in the 50s and stocks were flat during your formative years, it’s likely you are more inclined towards owning guaranteed/fixed investments like CDs or annuities, or maybe to not investing at all. If you were born in the 60s and saw high inflation during your formative years, you might be much more willing to take investment risk, since you feel that everything is always getting more expensive at a rate way above what returns you can get in those guaranteed/fixed CDs and annuities.

One decade apart, and two people with otherwise similar financial lives (same location, same income, etc.) can make opposite decisions about their money. Each may think the other is crazy. Housel is trying to show that while there are definitely bad/wrong financial decisions, and maybe even some decisions that are crazy (regardless of whether they work out or not), no one is crazy.

Every financial decision a person makes, makes sense to them in that moment and checks the boxes they need to check. They tell themselves a story about what they’re doing and why they’re doing it, and that story has been shaped by their own unique experiences. (Page 18)

Before we take this wisdom to better understand the financial decisions of our friends or spouse, we should first look in the mirror. We need to first acknowledge we have a history with money, some aspects very individual to our lives like whether our parents were wealthy or poor or neither, and some aspects influenced by the broader economic situation of our formative years. Togethers these don’t determine our decisions, but they influence them enough that we need to attempt to identify them, and even use them to our advantage.

So next time you’re in for a review, don’t be startled or confused if we ask you something like “What’s your earliest memory of money?” What do you remember about the U.S. economy during your teens and twenties?

Knowing the answers to these questions will help us as the guide and you as the hero on your journey of financial success.

Until next time, happy reading!